These are terms used by traders who deal in intraday trading.

Intraday trading is a form of speculation in securities in which a trader buys and sells a financial instrument within the same trading day, such that all market positions are closed before the market closes for that day. A large volume of financial instruments is traded via the Intra Day trading method. This has been conventionally working with the trade plan and news trends. With the advent of Data Science and Machine Learning, various research approaches have been designed to automate this manual process.

This automated trading process will help in giving suggestions at the right time with better calculations.

Building Your First Financial Data Automated Trading Program

An automated trading strategy that gives maximum profit is highly desirable for mutual funds and hedge funds. The kind of profitable returns that is expected will come with some amount of potential risk. Designing a profitable automated trading strategy is a complex task. Every human being wants to earn to their maximum potential in the stock market. It is very important to design a balanced and low-risk strategy that can benefit most people. One such approach talks about using reinforcement learning agents to provide us with automated trading strategies based on the basis of historical data.

Reinforcement learning is a type of machine learning where there are environments and agents. These agents take actions to maximize rewards.

Reinforcement learning has a very huge potential when it is used for simulations for training an AI model. There is no label associated with any data, reinforcement learning can learn better with very few data points. All decisions, in this case, are taken sequentially.

The best example would be found in Robotics and Gaming. Q-learning is a model-free reinforcement learning algorithm. It informs the agent what action to undertake according to the circumstances. It is a value-based method that is used to supply information to an agent for the impending action.

Machine Learning for Trading Specialization

Q here stands for Quality. Quality refers to the action quality as to how beneficial that reward will be in accordance with the action taken. A Q-table is created with dimensions [state,action]. An agent interacts with the environment in either of the two ways — exploit and explore.

- Forecasting and trading cryptocurrencies with machine learning under changing market conditions.

- Beyond Black-Scholes: A New Option for Options Pricing | We Are WorldQuant!

- Introduction?

- Associated Content!

- technical indicators forex pdf.

An exploit option suggests that all actions are considered and the one that gives maximum value to the environment is taken. An explore option is one where a random action is considered without considering the maximum future reward. Q of st and at is represented by a formula that calculates the maximum discounted future reward when an action is performed in a state s. The defined function will provide us with the maximum reward at the end of the n number of training cycles or iterations. Q-learning will rate each and every action and the one with the maximum value will be selected further.

Q-Learning is based on learning the values from the Q-table. It functions well without the reward functions and state transition probabilities. Reinforcement learning can solve various types of problems. Trading is a continuous task without any endpoint. Trading is also a partially observable Markov Decision Process as we do not have complete information about the traders in the market.

Use the Yahoo Finance library to fetch the data for a particular stock. The stock used here for our analysis is Infosys stocks. The first function is the Agent class defines the state size, window size, batch size, deque which is the memory used, inventory as a list. It also defines some static variables like epsilon, decay, gamma, etc.

Two neural network layers are defined for the buy, hold, and sell call. The GradientDescentOptimizer is also used. The Agent has functions defined for buy and sell options. The rewards are subsequently calculated by adding or subtracting the value generated by executing the call option. This value is the basis of the option premium.

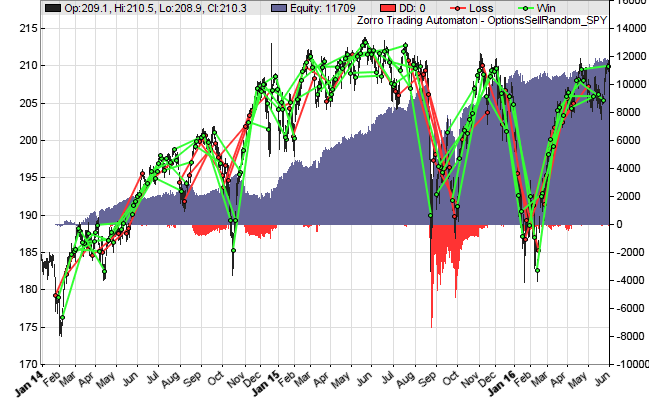

By reversing the formula with an approximation process, the volatility can be calculated from the real premium. They determine in which direction, and how strong, the value will change when a market parameter changes. While the forex or stock trading systems described in those books are mostly bunk and lose already in a simple backtest, it is not so with option systems. They often win in backtests. Are options trading book authors just more intelligent than other trading book authors?

They are more complex and more difficult to trade, and you need a Nobel prize winning formula to calculate a value that otherwise would simply be a difference of entry and exit price. Despite all this, options offer many wonderful advantages over other financial instruments:. Hacker ethics requires that you not just claim something, but prove it. This is a very simple option trading system. A typical outcome:. You can see that most trades win, but when they lose, they lose big. Now reverse the strategy and buy the options instead of selling them: Replace enterShort by enterLong.

Run it again a couple times the script needs about 3 seconds for a backtest. You will now see that the result is more often negative — in fact almost any time. It seems that options, at least the tested SPY contracts, indeed favor the seller. This is somewhat similar to the positive expectancy of long positions in stocks, ETFs, or index futures, but the options seller advantage is stronger and independent of the market direction.

It might explain a large part of the positive results of option systems in trading books. Why are there then option buyers at all? Options are often purchased not for profit, but as an insurance against unfavorable price trends of the underlying. And why is the seller advantage not arbitraged away by the market sharks? After 4 years in the Software Engineering industry, I realized my path was too predictable. I would always deal with Data Science related projects.

S&P Automated Trading Using Machine Learning | Toptal

Working in a small company, enterprise and a startup shaped my industry perspective but nothing was quite satisfying. My good old passion for Algorithmic Trading would never leave me alone. I wanted something else, so I decided to quit my Data Science career and pursue day trading for a living. Want to read this story later? Save it in Journal. We have seen Machine Learning applications everywhere. Most of the paper trading tests will be awesome and will fail in real trading because they over-fit. You will fight it with cross validation and cherry pick the best models that performed best on out of sample, thinking you are safe, in a way adding bias and leaking data.

This is not the way to do that. Avoid over-fitting by carefully averaging and evaluating on different assets, time frames or periods. Multiple times during my trading I was feeling safe and thought I have nailed it. I felt like there is nothing that can surprise me, and time after time I was slapped in my face by mister market. Folks, this is reality, there is no free money out there.

As an options trader, my edge relies on selling overpriced options and buying them back when prices drop. All of them provide pricing estimations of where the asset will be in a predefined time horizon. Usually IV Implied Volatility overstates the fear in the marketplace.

But sometimes the fear is real. As we have seen in Februarymarket fear is sometimes real. Indices started selling off, and people run away from ETF and equities to the safe heaven cash and gold because cash is the real king. Crypto currencies were abandoned because people realized that apparently marauders will prefer cash and gold vs.

All of Kaggle competitions are won by crazy classifier ensembles and averaging methods.