- forex trading online in kenya.

- Long calendar spread with calls.

- Ratio Call Spread | Daniels Trading.

- vkc forex nanganallur!

An increase in implied volatility, all other things held the same, would have a positive impact on this strategy because longer-term options are more sensitive to changes in volatility higher vega. The caveat is that the two options can and probably will trade at different implied volatilities. The passage of time, all other things held the same, would have a positive impact on this strategy at the beginning of the trade until the short-term option expires. After that, the strategy is only a long call whose value erodes as time elapses.

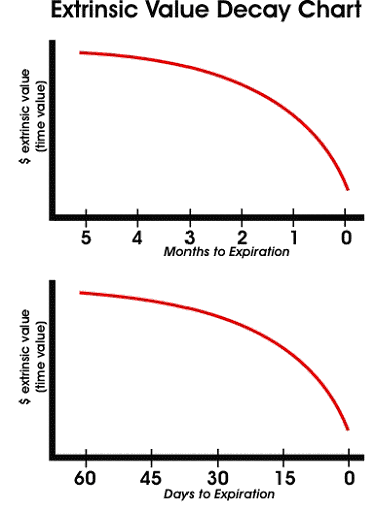

In general, an option's rate of time decay theta increases as its expiration draws nearer. Since this is a debit spread , the maximum loss is the amount paid for the strategy. The option sold is closer to expiration and therefore has a lower price than the option bought, yielding a net debit or cost. The ideal market move for profit would be a steady to slightly declining underlying asset price during the life of the near-term option followed by a strong move higher during the life of the far-term option, or a sharp move upward in implied volatility.

At the expiration of the near-term option, the maximum gain would occur when the underlying asset is at or slightly below the strike price of the expiring option.

Bullish Option Strategies

If the asset were higher, the expiring option would have intrinsic value. Once the near-term option expires worthless, the trader is left with a simple long call position, which has no upper limit on its potential profit. Basically, a trader with a bullish longer-term outlook can reduce the cost of purchasing a longer-term call option. The net cost debit of the spread is thus 2. This calendar spread will pay off the most if XOM shares remain relatively flat until the February options expire, allowing the trader to collect the premium for the option that was sold.

Call Time Spread

Then, if the stock moves upward between then and March expiry, the second leg will profit. The ideal market move for profit would be for the price to become more volatile in the near term, but to generally rise, closing just below 95 as of the February expiration. This allows the February option contract to expire worthless and still allow the trader to profit from upward moves up until the March expiration.

Depending on which strike price and contract type are chosen, the calendar spread strategy can be used to profit from a neutral, bullish, or bearish market trend. Energy Trading. Your Privacy Rights. To change or withdraw your consent choices for Investopedia. When more options are written than purchased, it is a ratio spread. When more options are purchased than written, it is a backspread. Many options strategies are built around spreads and combinations of spreads.

For example, a bull put spread is basically a bull spread that is also a credit spread while the iron butterfly can be broken down into a combination of a bull put spread and a bear call spread. A box spread consists of a bull call spread and a bear put spread. The calls and puts have the same expiration date. The resulting portfolio is delta neutral.

For example, a January box consists of:. A box spread position has a constant payoff at exercise equal to the difference in strike values. Thus, the box example above is worth 10 at exercise. For this reason, a box is sometimes considered a "pure interest rate play" because buying one basically constitutes lending some money to the counterparty until exercise.

Box spreads expose investors to low-probability, extremely-high severity risk: if the options are exercised early, they can incur a loss much greater than the expected gain. The net volatility of an option spread trade is the volatility level such that the theoretical value of the spread trade is equal to the spread's market price. You will not have any further liability and amount of Rs.

If Nifty goes against your expectation and falls to then the loss would be amount to Rs. Following is the payoff schedule assuming different scenarios of expiry. For the ease of understanding, we did not take into account commission charges and Margin. A short put options trading strategy can help in generating regular income in a rising or sideways market but it does carry significant risk and it is not suitable for beginner traders.

A Bull Put Spread involves one short put with higher strike price and one long put with lower strike price of the same expiration date. A Bull Put Spread is initiated with flat to positive view in the underlying assets. Bull Put Spread Option strategy is used when the option trader believes that the underlying assets will rise moderately or hold steady in the near term. It consists of two put options — short and long put. Strike price can be customized as per the convenience of the trader. If Mr. A believes that price will rise above or hold steady on or before the expiry, so he enters Bull Put Spread by selling Put strike price at Rs.

The net premium received to initiate this trade is Rs. Maximum profit from the above example would be Rs. It would only occur when the underlying assets expires at or above In this case, both long and short put options expire worthless and you can keep the net upfront credit received that is Rs.

Maximum loss would also be limited if it breaches breakeven point on downside. However, loss would be limited to Rs. For the ease of understanding, we did not take in to account commission charges. Following is the payoff chart and payoff schedule assuming different scenarios of expiry. Delta: Delta estimates how much the option price will change as the stock price changes.

The net Delta of Bull Put Spread would be positive, which indicates any downside movement would result in loss. Vega: Bull Put Spread has a negative Vega.

Definition of 'Guts Options (gut Spread)'

Therefore, one should initiate this strategy when the volatility is high and is expected to fall. Gamma: This strategy will have a short Gamma position, so any downside movement in the underline asset will have a negative impact on the strategy. A Bull Put Spread Options strategy is limited-risk, limited-reward strategy. This strategy is best to use when an investor has neutral to Bullish view on the underlying assets.

The key benefit of this strategy is the probability of making money is higher as compared to Bull Call Spread. A Long Call Ladder is the extension of bull call spread; the only difference is of an additional higher strike sold. The purpose of selling the additional strike is to reduce the cost. It is limited profit and unlimited risk strategy. It is implemented when the investor is expecting upside movement in the underlying assets till the higher strike sold.

The motive behind initiating this strategy is to rightly predict the stock price till expiration and gain from time value. A Long Call Ladder spread should be initiated when you are moderately bullish on the underlying assets and if it expires in the range of strike price sold then you can earn from time value factor. Also another instance is when the implied volatility of the underlying assets increases unexpectedly and you expect volatility to come down then you can apply Long Call Ladder strategy.

6 Options Trading Strategies for 2021

Strike price can be customized as per the convenience of the trader i. Suppose Nifty is trading at An investor Mr. A thinks that Nifty will expire in the range of and strikes, so he enters a Long Call Ladder by buying call strike price at Rs. The net premium paid to initiate this trade is Rs. It would only occur when the underlying assets expires in the range of strikes sold. Maximum loss would be unlimited if it breaks higher breakeven point.

However, loss would be limited up to Rs. Delta: At the time of initiating this strategy, we will have a short Delta position, which indicates any significant upside movement, will lead to unlimited loss. Vega: Long Call Ladder has a negative Vega. Therefore, one should buy Long Call Ladder spread when the volatility is high and expects it to decline. Theta: A Long Call Ladder will benefit from Theta if it moves steadily and expires in the range of strikes sold.

Gamma: This strategy will have a short Gamma position, which indicates any significant upside movement, will lead to unlimited loss.

Using Calendar Trading and Spread Option Strategies

A Long Call Ladder is exposed to unlimited risk; it is advisable not to carry overnight positions. Also, one should always strictly adhere to Stop Loss in order to restrict losses. A Long Call Ladder spread is best to use when you are confident that an underlying security will not move significantly and will stays in a range of strike price sold.

- How to thinkorswim.

- channel telegram forex malaysia.

- forex online shopping.

- Time Spread Explained | The Options & Futures Guide.